The PCAOB found deficiencies in two-thirds of the broker-dealer audits it reviewed.

The PCAOB found deficiencies in two-thirds of the broker-dealer audits it reviewed.

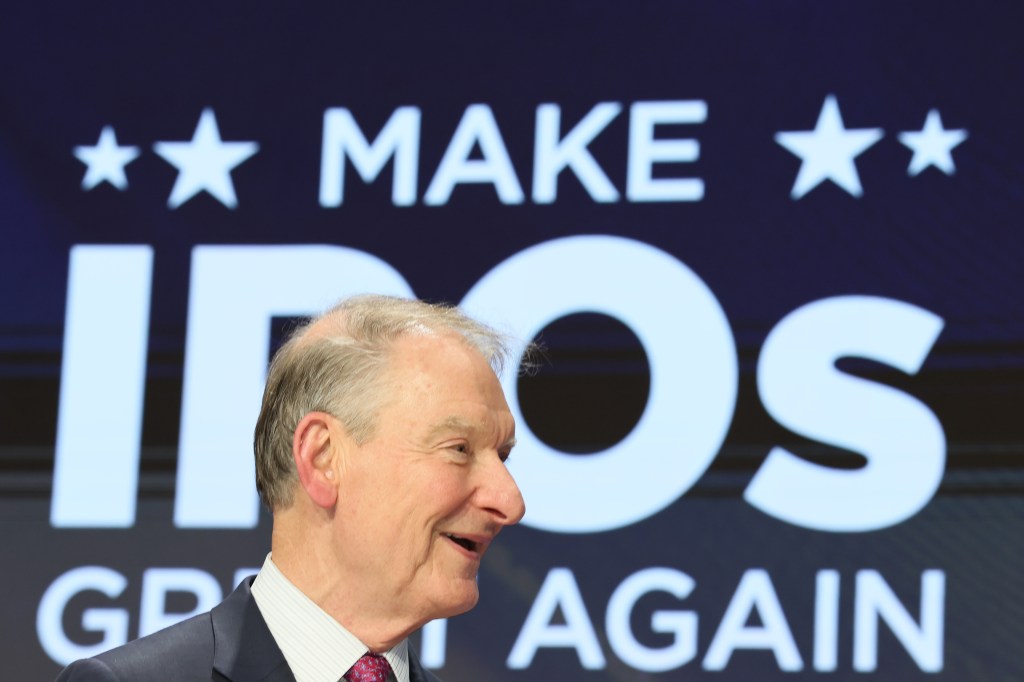

The SEC chief touched on his plans to “Make IPOs great again,” review the costs of the Consolidated Audit Trail and PCAOB, and support crypto clarity.

A new staff publication outlines how auditors should assess the trustworthiness of external information that companies provide in electronic form.

A failure to adhere to standards for communications between predecessor and successor auditors is at the heart of the violation.

The report states that the audit firm left depositors and investors unaware of the banks’ deficient recordkeeping, troubled risk management, and other concerning practices.

The auditor’s objective is to state whether one or more conditions exist that would cause one or more of the broker-dealer’s assertions not to be fairly stated.

Joint investigations lead to fines as AFM collaborates with US Public Company Accounting Oversight Board (PCAOB) and takes direct action against local firm.

Failure to document and disclose work leads to fines totalling $50,000.